All Categories

Featured

Table of Contents

Life insurance covers the insured person's life. If you pass away while your policy is energetic, your recipients can use the payment to cover whatever they choose clinical costs, funeral costs, education, financings, everyday expenses, and even financial savings.

Depending on the problem, it might impact the plan kind, price, and protection amount an insurer offers you. Life insurance policy plans can be classified right into three primary teams, based on just how they function:.

Policyholders

OGB offers two fully-insured life insurance plans for workers and retirees through. The state shares of the life insurance policy costs for covered staff members and retirees. Both strategies of life insurance coverage available, in addition to the equivalent quantities of dependent life insurance policy supplied under each plan, are kept in mind below.

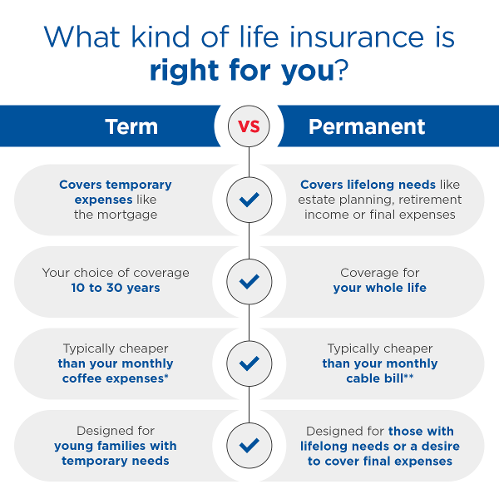

Term Life insurance is a pure transference of threat in exchange for the repayment of costs. Prudential, and prior carriers, have been providing insurance coverage and assuming threat for the payment of costs. In case a covered person were to pass, Prudential would recognize their obligation/contract and pay the benefit.

Strategy members presently enrolled who want to include dependent life protection for a spouse can do so by providing proof of insurability. Worker pays 100 percent of reliant life costs.

Agreement Series: 83500. 2018 Prudential Financial, Inc. and its associated entities. Prudential, the Prudential logo, the Rock sign, and Bring Your Obstacles are service marks of Prudential Financial, Inc. and its relevant entities, signed up in lots of jurisdictions worldwide. 1013266-00001-00.

Living Benefits

The price structure enables employees, spouses and cohabitants to pay for their insurance policy based on their ages and chosen protection amount(s). The maximum assured issuance amount available within 60 days of your hire date, without proof of insurability is 5 times your base yearly income or $1,000,000, whichever is less.

While every attempt has been made to make sure the precision of this Recap, in case of any disparity the Recap Strategy Summary and Strategy Record will prevail.

Yet what happens when the unanticipated comes at you while you're still alive? Unexpected diseases, long-lasting handicaps, and more can strike without warning and you'll wish to prepare. You'll want to make sure you have options offered just in case. Fortunately for you, lots of life insurance policy policies with living advantages can provide you with financial support while you're alive, when you need it the most.

, yet the benefits that come with it are part of the reason for this. You can add living benefits to these plans, and they have money value development possibility over time, meaning you may have a few different alternatives to utilize in instance you need funding while you're still to life.

What types of Protection Plans are available?

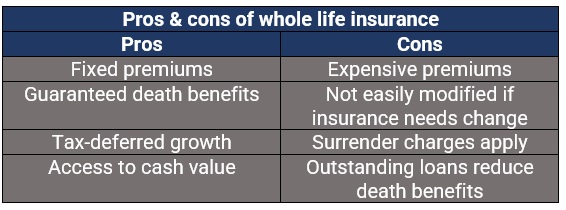

These policies might allow you to add particular living benefits while also allowing your strategy to accumulate cash worth that you can take out and utilize when you need to. is similar to entire life insurance coverage because it's a long-term life insurance coverage policy that implies you can be covered for the remainder of your life while enjoying a policy with living advantages.

When you pay your premiums for these plans, part of the repayment is drawn away to the cash money value. This money worth can expand at either a dealt with or variable price as time progresses depending on the kind of policy you have. It's this quantity that you might have the ability to access in times of need while you live.

The disadvantage to using a withdrawal is that it can raise your costs or lower your fatality advantage. Surrendering a plan basically indicates you've terminated your policy outright, and it automatically provides you the money value that had accumulated, much less any surrender fees and outstanding plan expenditures.

Using cash money value to pay costs is essentially simply what it appears like. Relying on the kind of plan, you can make use of the money worth that you have actually built up with your life insurance policy to pay a portion or all your premiums. A living benefit rider is a kind of life insurance biker that you can include in your life insurance plan to make use of in your lifetime.

What does Protection Plans cover?

The terms and quantity available will certainly be specified in the policy. Any type of living advantage paid from the fatality advantage will certainly decrease the quantity payable to your beneficiary (Policyholders). This payment is suggested to aid provide you with comfort for completion of your life in addition to aid with medical costs

Essential illness cyclist ensures that benefits are paid straight to you to spend for therapy solutions for the health problem specified in your plan agreement. Long-term care bikers are established to cover the cost of in-home care or assisted living home costs as you grow older. A life negotiation is the procedure where you sell a life insurance coverage plan to a 3rd party for a round figure repayment.

Who are the cheapest Riders providers?

That depends. If you remain in an irreversible life insurance policy policy, after that you're able to withdraw cash money while you live via finances, withdrawals, or surrendering the policy. Before deciding to use your life insurance policy policy for money, get in touch with an insurance agent or representative to figure out how it will certainly affect your recipients after your fatality.

All life insurance coverage plans have one thing in common they're made to pay money to "named recipients" when you die. Life insurance policy plans can be taken out by partners or any individual that is able to confirm they have an insurable rate of interest in the individual.

Who provides the best Level Term Life Insurance?

The policy pays cash to the named beneficiaries if the insured passes away during the term. Term life insurance policy is meant to supply lower-cost insurance coverage for a specific duration, like a 10 year or 20-year period. Term life plans might include a provision that enables insurance coverage to continue (renew) at the end of the term, also if your health condition has actually changed.

Ask what the premiums will certainly be prior to you renew. Ask if you shed the right to restore at a certain age. If the plan is non-renewable you will certainly need to obtain insurance coverage at the end of the term. is different since you can maintain it for as long as you require it.

{kind=link}

Table of Contents

Latest Posts

Why do I need Life Insurance Plans?

What is Joint Term Life Insurance? Your Essential Questions Answered?

What is the difference between Level Term Life Insurance Benefits and other options?

More

Latest Posts

Why do I need Life Insurance Plans?

What is Joint Term Life Insurance? Your Essential Questions Answered?

What is the difference between Level Term Life Insurance Benefits and other options?